{kind=link}

Federal reserve decisions always sneak up on me like that unexpected bill in the mail, y’know? I’m sitting here in my cramped apartment in Chicago—it’s December 29, 2025, snow piling up outside my window, coffee going cold on the desk—and I’m refreshing news tabs about the latest Fed move from earlier this month. Seriously, these federal reserve decisions hit my wallet harder than that time I impulse-bought those concert tickets last summer.

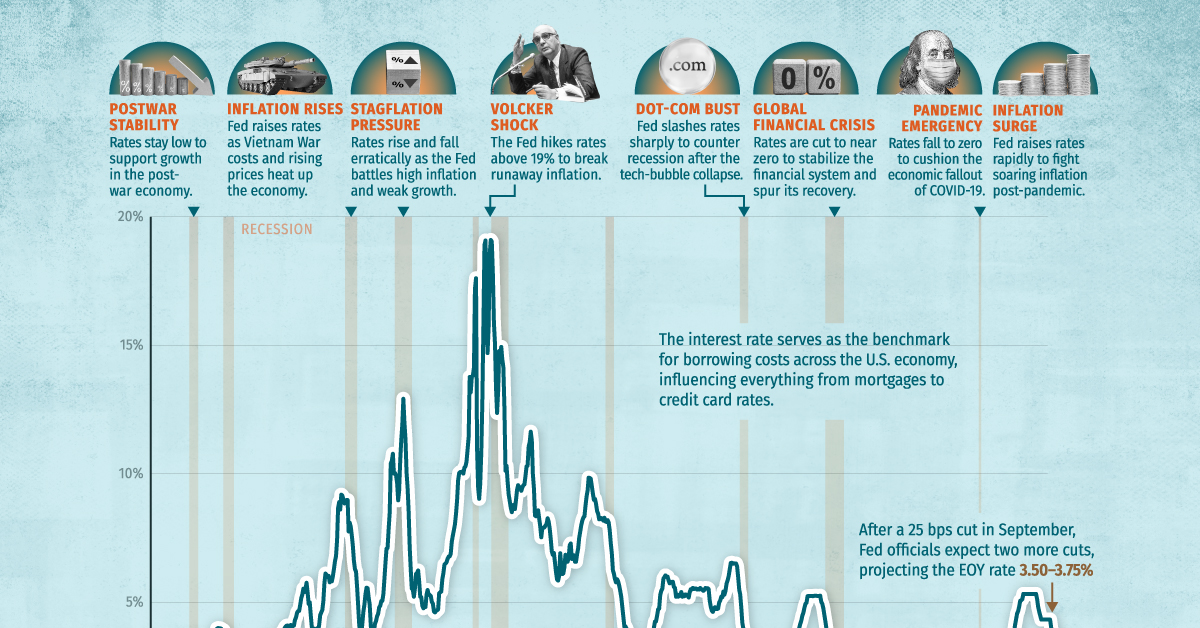

Back in December, the Fed cut rates again—for the third time this year—dropping the federal funds rate to 3.5%-3.75%. I remember watching Powell’s press conference on my phone while eating leftover takeout, thinking, “Okay, this might actually help my credit card debt breathe a little.” But honestly? It’s bittersweet. My variable-rate cards dipped a tad, but I’m still paying way more interest than I should because I racked up balances during those high-rate years. Embarrassing admission: I once ignored the hikes and kept swiping for “just one more” Uber Eats order. Lesson learned the hard way.

How Federal Reserve Decisions Mess With My Borrowing Costs

Look, when the Fed tweaks interest rates, it’s like they’re remotely controlling the price of everything I borrow. Higher rates? Everything gets pricier. Lower? A bit of relief. That December cut was a quarter-point, part of bringing things down from the peaks. But federal reserve decisions aren’t instant magic—my auto loan from last year is still stinging.

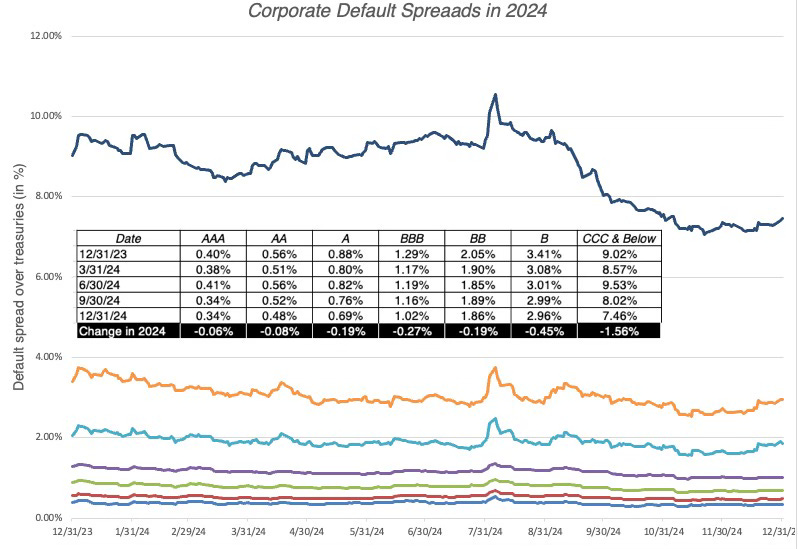

- Credit cards: Mine are variable, tied to prime rate, which follows Fed moves. After the cuts, my APR dropped maybe half a percent. Not life-changing, but it shaved $20 off my minimum payment. Win?

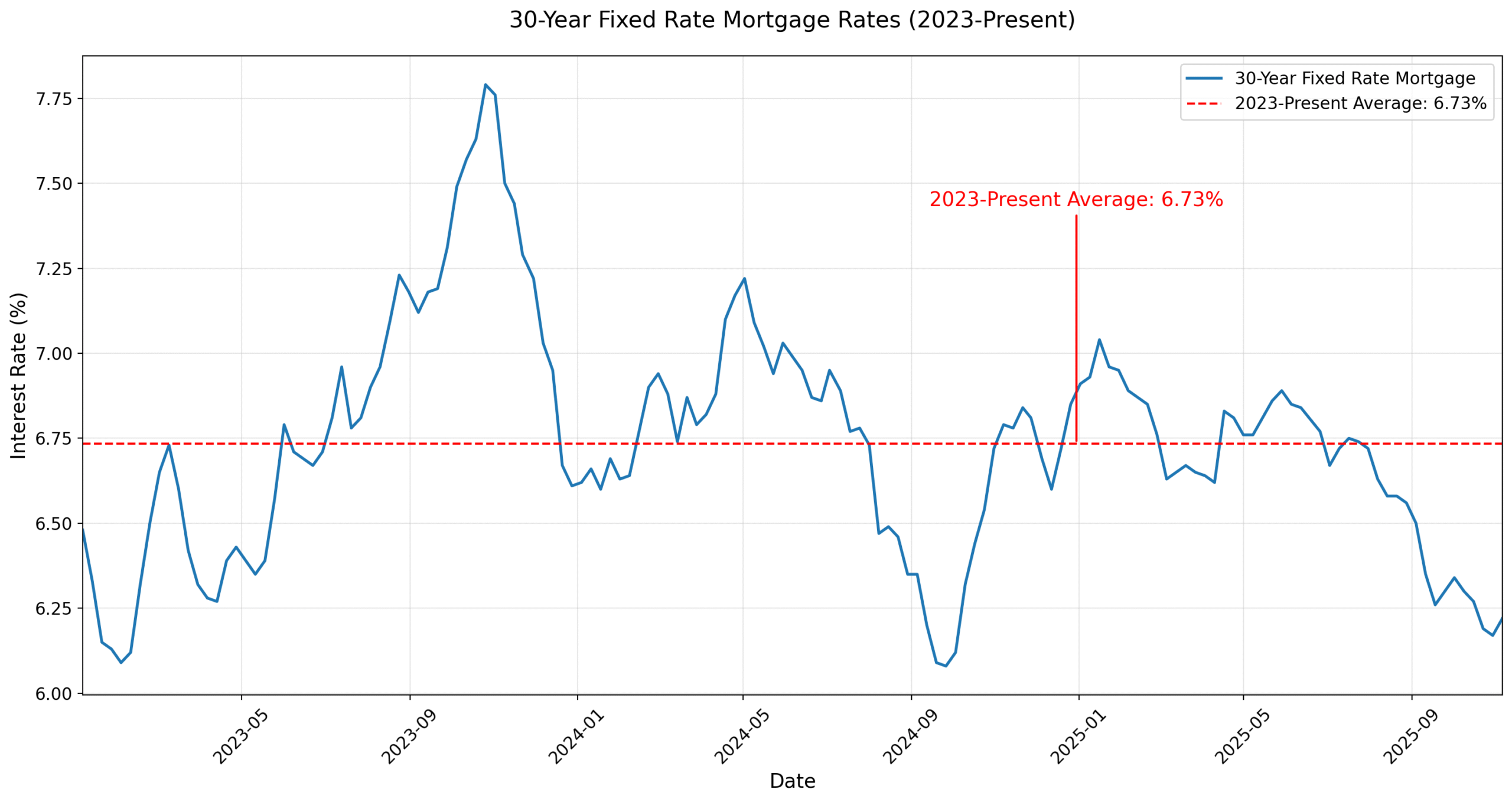

- Mortgages: I’ve been eyeing homes, and lower Fed rates pushed 30-year fixed down nearer to 6%. Still high compared to pre-2022, but better than 8%. Anyway, I’m debating refinancing my old one—fingers crossed.

This is basically me every month when the statement arrives. Raw honesty: Federal reserve decisions amplified my bad habits back when rates were skyrocketing—I should’ve paid down debt faster.

Federal Reserve Decisions and My Savings (Or Lack Thereof)

On the flip side, lower federal reserve decisions mean my high-yield savings account isn’t earning as much anymore. I finally started one this year after reading too many Reddit threads, and it was hitting 5%+ during peaks. Now? Closer to 4%. Still beats regular banks, but ouch.

But hey, contradictions abound—I’m cautiously optimistic because cheaper borrowing might let me consolidate debt or finally build that emergency fund without feeling squeezed. According to the official Fed statement, they’re watching risks to employment and inflation carefully (source: https://www.federalreserve.gov/newsevents/pressreleases/monetary20251210a.htm).

Charts like these keep me grounded—rates are down from 2024 highs, but the dot plot shows maybe just one more cut in 2026. No wild drops ahead.

What the Latest Federal Reserve Decisions Mean for Home Buying Dreams

Federal reserve decisions are why I’m suddenly house-hunting again. Lower rates = lower monthly payments. I crunched numbers: On a $300k loan, that quarter-point cut saves like $50/month. Adds up!

This could be me soon—shaking hands, getting keys. But I’m flawed; I got pre-approved once before and chickened out when rates spiked. Learning process, right?

And this beast in DC is where it all happens. Feels distant from my Midwest life, but federal reserve decisions ripple straight to my bank app.

Anyway, my unfiltered take: These Fed moves are helpful but slow. I messed up by not acting sooner on debt, but now I’m paying extra principals when I can. Tip from my mistakes—track rates via sites like Bankrate or the Fed’s own page, and don’t wait for perfect timing.

Wrapping this chat—federal reserve decisions aren’t abstract; they’re in my grocery budget, my stress levels, my future plans. What’s your story with these rate changes? Drop a comment if you’re feeling the pinch (or relief) too. And seriously, check your own rates today—might save you some cash before the next meeting. Talk soon.